Preparing for a comfortable retirement by building wealth today

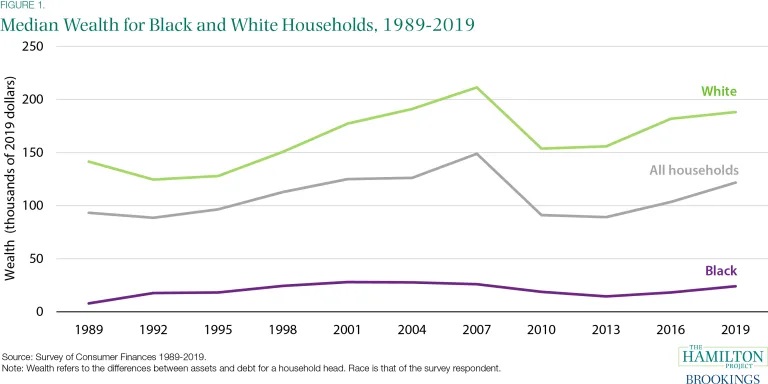

Like many pre-retirees in the U.S., saving enough money to retire is a top concern of Black Americans. In fact, 43% of Black Americans call it their top financial worry1 — the same percentage as all demographic segments combined. However, the net worth of a typical White family is nearly 10x greater than that of a Black family.2 And that wealth gap isn’t getting any better as time goes on.

Why is the wealth gap so large? The answer to this question isn’t simple. While companies like Equitable have a long history of building financial empowerment in minority communities, a lack of financial education, financial literacy and opportunity puts the Black community at a severe disadvantage. In addition, investor behavior may also play a part in the wealth gap. Specifically, data shows that Black individuals tend to take larger risks to try and achieve their financial goals, like investing in cryptocurrency,3 and may also start out their careers with more student loan debt than their White counterparts.6

While there may be challenges to overcome, Black families with the right tools and resources – including an educated financial professional – can help close the wealth gap and build wealth for themselves and generations to come.

Taking risks and protecting wealth

Studies show that Black families who want financial independence and wealth tend to over-rely on high-risk investments, like house flipping, stock investments and starting a business to help accomplish their goals. While is it encouraging that Black stock ownership is growing3 and Black individuals and immigrants are almost twice as likely to start a business as whites4, these types of investments carry more risk of loss than other types of investments. For that reason, it’s important to take a holistic approach to financial planning and include protection products as well.

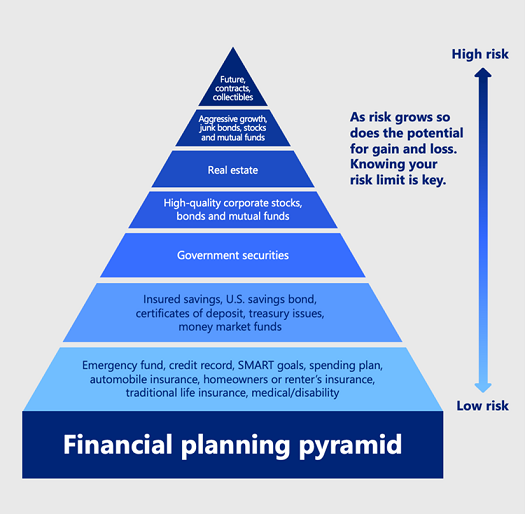

The financial planning pyramid

As you can see from this graphic, a well-rounded financial plan can include a wide variety of investments, from life insurance all the way up to futures and collectibles. As the risk of these investments grows, so does the potential for gain and loss. That’s why it’s important to start at the bottom of the pyramid and continue building assets upwards to help keep the pyramid steady and your financial plans in line with your long term goals.

Managing debt is part of it too

Part of a successful financial plan is managing the amount of debt you carry. According to research, Black Americans are more likely to be concerned about paying off or reducing student loan debt than the general population.1 However, that may be because they have more debt than other demographics.

For example, Black and African American college graduates owe an average of $25,000 more in student loan debt than White college graduates.5 That amount of debt can be crushing to a new career and can keep young workers from making forward progress in their financial plans. At 46%, Black student borrowers were the most likely to put off buying a home.5And, at 43%, Black indebted student borrowers are also the most likely to report having to work more than they would prefer.5

Managing debt can be complicated and, at times, overwhelming to anyone. Leaning on an experienced financial professional is a good step, as they can help you find opportunities to consolidate your loans and establish a budget that may let you pay off your debt more quickly.

Wealth is built over time and generations

While systemic inequalities have prevented many Black Americans from saving and building wealth, there are actions you can take to help you grow your assets and build a more secure financial future.

Establish long-term savings goals.

According to research, Black Americans understand the need to save for long-term goals. Specifically, 44% are concerned about being able to save money for an emergency fund and 43% are concerned about having enough money for a comfortable retirement.1 If this sounds like you, take steps today to achieve both short- and long-term saving goals. Even small steps can help get you started.

Embrace the power of compounding interest.

Consider investing in products or strategies that allow you to defer taxes until some later date when your tax bracket may be lower. For example, qualified retirement plans like 401(k) and 403(b) plans, traditional IRAs and annuities are all tax-deferred savings vehicles. So instead of paying taxes on earnings each year, your earnings are allowed to grow and compound (earning interest of their own) over time. In contrast, you will pay taxes on earnings each year in a taxable account, which can take a bite out of your savings each year.

Use life insurance to help build generational wealth.

Having a life insurance policy can help you protect your family from financial hardship should something happen to you unexpectedly. Depending on the kind of life insurance you buy, it can also allow for the potential to build cash value during your lifetime, giving you the option to access the funds via withdrawals or loans to pay for retirement, medical, or unexpected expenses while you’re still alive.**

Find an experienced financial professional.

Making informed decisions about your future starts with putting a plan in place. If you’re not sure where to begin, consider finding a financial professional who can work with you to get to know you and understand your situation, build on your existing assets, and help you learn about the options that are available to you. Someone who will be ready with answers to your questions and clear recommendations to help you achieve your goals. When you team up with a financial professional, you can feel confident that your plans are on track at every stage of life.

Equity. It’s in our name.

If you’re not sure where to start, consider a company who has a long history of being a trusted bastion of support for Black families and communities.

Equitable has a diverse coalition of financial professionals to support, guide and stand behind Black Americans of all generations. If you don’t have a financial professional, consider one from Equitable.

** Policy loans and withdrawals will reduce the cash value and death benefit of the contracts. Clients may need to fund higher premiums in later years to keep the policy from lapsing. Under current federal tax rules, you generally may take income tax-free partial withdrawals under a life insurance policy that is not a modified endowment contract (MEC), up to your basis in the contract. Additional amounts are includible in income. The IRS places a limit on how much money can go into life insurance premiums for the policy and how quickly such premiums can be paid in order for the policy to retain all of its tax benefits. If certain limits are exceeded, a MEC results. MEC policyholders may be subject to taxes on distributions on an income-first basis, that is, to the extent there is gain in their policies, as well as penalties on any taxable amount if they are not age 59 1/2 or older. Loans taken will be free of current income tax as long as the policy remains in effect until the insured’s death, does not lapse and is not a MEC. Please note that outstanding loans accrue interest. Income tax-free treatment also assumes the loan will eventually be satisfied from income tax-free death benefit proceeds. Loans and withdrawals reduce the policy’s cash value and death benefit, may cause certain policy benefits or riders to become unavailable and may increase the chance the policy may lapse. If the policy lapses, is surrendered or becomes a MEC, the loan balance at such time would generally be viewed as distributed and taxable under the general rules for distribution of policy cash values. In addition, withdrawals, policy loans and any accrued loan interest may cause your policy to lapse even if you are in a period of coverage under the No-Lapse Guarantee Rider. Speak to your financial professional before taking any withdrawals or policy loans.

Life insurance is issued by Equitable Financial Life Insurance Company (Equitable Financial), New York, NY 10104; or by Equitable Financial Life Insurance Company of America (Equitable America), an Arizona Stock Corporation, with main administrative office in Jersey City, NJ. Equitable America is not licensed to conduct business in New York.) It is distributed by Equitable Network (Equitable Network Insurance Agency of California in CA; Equitable Network Insurance Agency of Utah in UT; Equitable Network of Puerto Rico, Inc. in PR), LLC and Equitable Distributors, LLC. Variable life insurance is co-distributed by Equitable Advisors, LLC (member FINRA, SIPC) (Equitable Financial Advisors in MI and TN) and Equitable Distributors, LLC. When sold by New York state-based (i.e., domiciled) Financial Professionals, life insurance is issued by Equitable Financial Life Insurance Company (New York, NY). Securities offered through Equitable Advisors, LLC (NY, NY 212-314-4600), member FINRA, SIPC (Equitable Financial Advisors in MI & TN). Annuity and insurance products offered through Equitable Network, LLC.

GE- 4721140.1 (5/22) (Exp.5/24)

![]()