As an educator, you have an advantage over many others when it comes to retirement readiness. You can look forward to a pension, which will provide you with a stream of income payments that will last as long as you live. A pension is a great foundation for retirement income, but it may not be enough to cover all your expenses in the future. You may need a greater percentage of your preretirement income than your pension will provide. If you happen to live in one of the states in which educators also receive Social Security, that extra monthly income will help. Even if you are covered by Social Security and a pension, your school district may offer the opportunity to increase your retirement savings through a 403(b) plan. To make sure you can retire confidently, you should consider the advantages of supplementing your pension by saving in a 403(b) plan.

Ready to take the next step?

Talk to a financial professional to open a 403(b) plan. |

Equitable clients can: |

What is a 403(b) plan?

A 403(b) is a tax-deferred savings plan for educators, similar to a 401(k) plan for private-sector workers. It is an optional savings plan offered by many school districts and can supplement your pension to help you prepare for and enjoy a more comfortable retirement. While your pension can help cover some essential expenses in retirement, it may not cover everything. A 403(b) plan can help support everything else, letting you enjoy the kind of retirement you want.

How does it work?

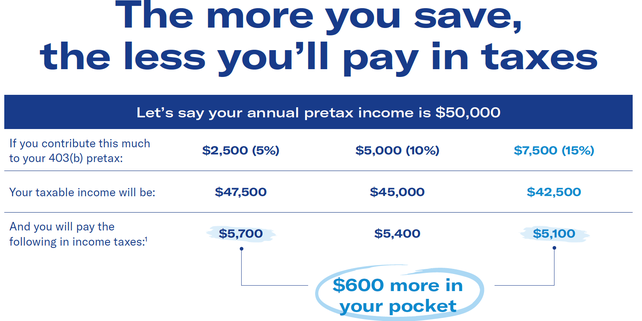

Much like a 401(k) plan, you contribute pretax money to a 403(b) plan through payroll deductions, you can choose from a variety of investments offered and your money has the opportunity to grow on a tax-deferred basis until you need it for retirement. Contributions to a 403(b) plan can also lower the federal income taxes withheld from your paycheck each pay period and reduce your annual taxable income.

- You can contribute $20,500 or more. In 2022, you can contribute up to $20,500 of your salary to a 403(b) plan. If you’re age 50 or older, you can add another $6,500. If you have worked at your school district for 15 years or more, you may also be entitled to an additional catch-up contribution.

- But you can start small and grow over time. You may not have $20,500 to contribute this year. That’s okay. With a 403(b) plan, you can start by contributing as much or as little as you want, and as your income grows or your situation changes over time, you can increase your contributions.

- You’ll select a variety of investments. Diversifying your investments can help you address the impact of the market’s ups and downs by reducing your risk of loss. That’s because not all investments react the same to economic, political or market conditions. If you’re not sure what to choose, you may want to consider working with a financial professional. They can help you design an investment strategy to meet your unique needs, goals and risk tolerance.

- Your money can grow tax-deferred. That means you won’t pay taxes on any earnings until you withdraw the money, typically when you’re retired and may be in a lower tax bracket.

Some 403(b) plans offer an annuity as an option, which can provide additional benefits

If your 403(b) plan offers an annuity, you may have additional investment benefits, such as:

- Guaranteed* income for the rest of your life, or for a specific period of time.

- Family protection through a guaranteed* death benefit.

- Options for professional investment management.

Feel more confident in the future

Make sure you know whether your district offers a 403(b) plan. Consider contacting a financial professional to explore the details and see if a 403(b) plan might be a good way to supplement your pension for retirement. With more ways to save and grow your money tax-deferred, it may help you worry less and gain more confidence in your future retirement.

Make sure a pension gap doesn’t impact your future vision. |

*All guarantees provided within annuities are based solely on the claims-paying ability of the issuing life insurance company. If you are purchasing an annuity contract to fund a qualified employer sponsored retirement arrangement, you should do so for the annuity’s features and benefits other than tax deferral. For such cases, tax deferral is not an additional benefit of the annuity. You may want to consider the relative features, benefits and costs of the annuity with any other investment that you may use in connection with your retirement plan or arrangement.

This informational and educational article does not offer or constitute investment, legal, tax accounting advice. Your unique needs, goals and circumstances require and deserve the individualized attention of your own financial, legal and tax professionals. Equitable Financial Life Insurance Company and its affiliates do not provide tax or legal advice or services.

Equitable is the brand name of the retirement and protection subsidiaries of Equitable Holdings, Inc., including Equitable Financial Life Insurance Company (Equitable Financial) (NY, NY), Equitable Financial Life Insurance Company of America (Equitable America), an AZ stock company with main administrative headquarters in Jersey City, NJ, and Equitable Distributors, LLC. The obligations of Equitable Financial and Equitable America are backed solely by their claims-paying abilities. Equitable Financial, Equitable America, Equitable Distributors and Equitable Advisors are affiliated companies and do not offer tax or legal advice.

![]()